Representative Example: You could borrow £10,699 over 60 months with an initial payment of £495.89 (including £199 Admin Fee) followed by 58 monthly payments of £296.89 with a final payment of £495.89 (including optional £199 Option to Purchase Fee). Total amount repayable will be £19,012,40. 26.1% APR, annual interest rate (fixed) 13.3%.

The Admin Fee is a £199 fee that helps cover the costs of setting up your finance agreement. It covers things like preparing your agreement documents, carrying out credit and identity checks, and arranging payment to the broker. This fee is paid at the same time as your first payment, and it isn't refundable. It's separate from your deposit and from any other charges on your agreement.

The Optional Purchase Fee is a £199 fee you only pay if you decide to buy the car at the end of your finance agreement. You don't have to buy the car, that's entirely your choice. If you choose to hand the car back instead, you won't pay this fee. If you decide to keep the car, you'll need to pay the £199 Optional Purchase Fee, usually along with your final payment, to transfer legal ownership of the vehicle to you. This fee covers the cost of finalising your agreement and removing our interest in the vehicle. It's separate from your deposit and from any other charges on your agreement.

The amount shown is an illustration of a typical monthly payment based on the Representative APR. These figures are for guidance only; the actual payments and rate you're offered will depend on your individual circumstances and are not guaranteed. Please see below for details of how your first and final payments may be different.

Applying for Car Finance with Bad Credit

If you’ve got bad credit and need a car, you might worry that finance isn’t an option. The good news is: many lenders offer car finance for people with poor credit, especially if you can show the loan is affordable.

In this guide, we’ll explain how your credit score affects your chances, what lenders check, and what options are available. We’ll also answer common questions like “Can I get car finance with very poor credit?” and “What is the minimum credit score needed to finance a car?”

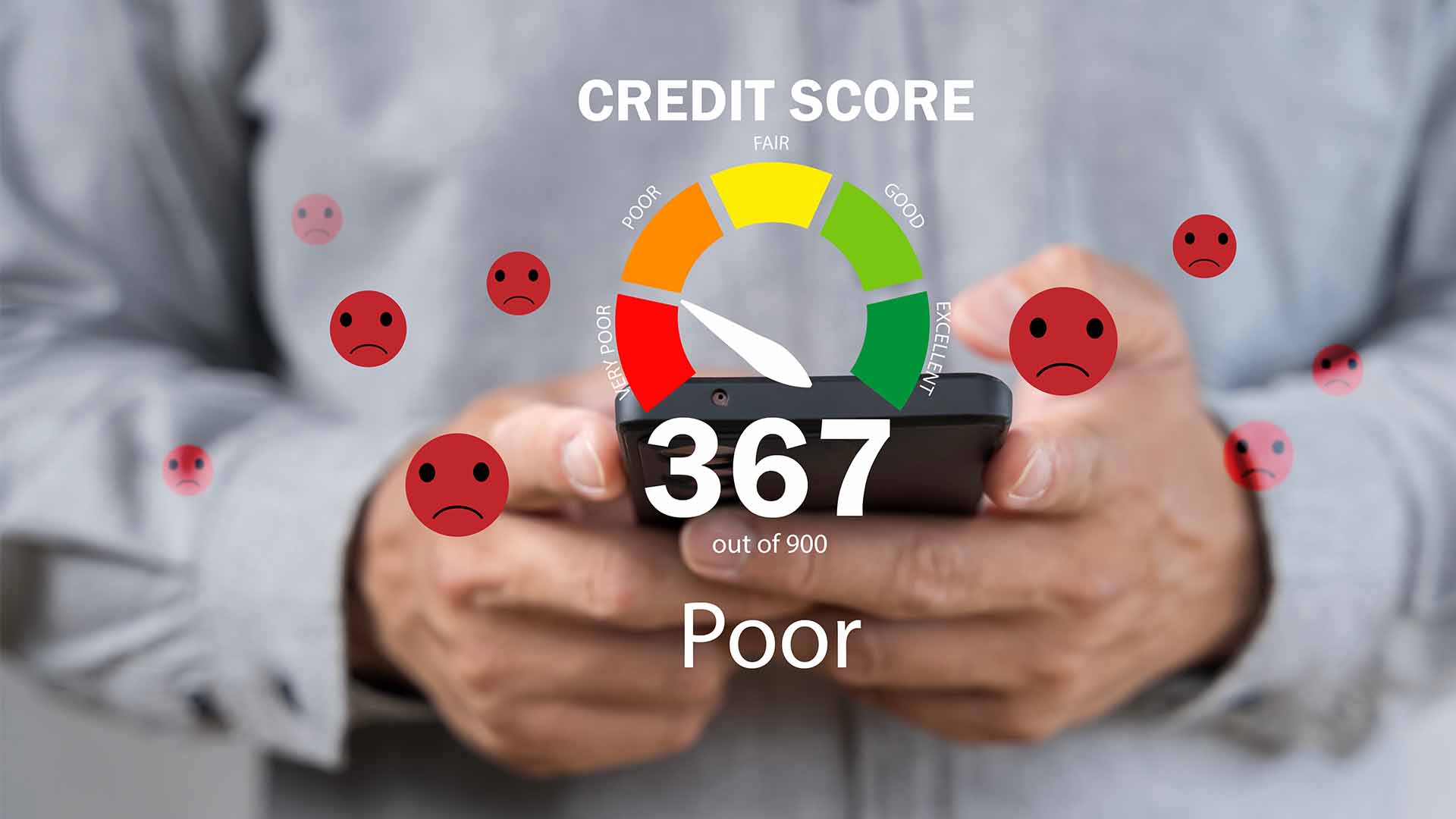

There’s no fixed number, but most lenders look for a score of 580 or more. Some will still consider you if your score is lower, especially bad credit lenders who use different rules.

A quick guide to credit score ranges:

Even with poor credit, you might still get approved, but you may be offered a higher interest rate, which could cost you more in the long run, so it's something to keep in mind.

Yes. Many lenders offer car finance for very poor credit, depending on your income, expenses, and how affordable the finance is.

To improve your chances:

Some lenders also give customers the option to apply with a guarantor or joint hirer, which can help support the application, for those with low credit scores.

Lenders do run checks, but each one is different. Some do a soft credit check first, which doesn’t affect your score, and then a hard check if you go ahead with the full application.

Lenders will usually check:

These checks are part of responsible lending rules. If you've been refused before, it doesn’t mean every lender will say no.

Your credit score plays a big role, but it's not the only thing lenders look at.

Other things that can affect your application:

You can look to improve your credit score by:

These small steps can gradually improve your credit score, and while you might not qualify for car finance right now, they could boost your chances in the future.

Even with a decent credit score, you might still be turned down. Wondering “Why am I being declined for car finance?” Here are some possible reasons:

If you’ve been declined by a lender directly, don’t worry, there may still be options available. Some lenders might accept your application if you apply with someone else, like a parent, guardian, partner, or relative, to support your application. Alternatively, you could use a finance broker to help find a lender that better matches your personal circumstances.

Your credit score affects how much interest you’ll pay. A lower score usually means higher rates, because lenders see you as more of a risk.

This could mean:

It’s important to compare offers and read the loan agreement carefully. Look at:

Even if your credit isn’t perfect, lenders should still offer fair terms. Don’t be afraid to ask questions if the finance offer seems too expensive or unclear.

Getting car finance is easier when you're prepared. Here’s what most lenders ask for:

Some lenders may also request:

If you’re offering a deposit, have proof ready too. Lenders use these documents to check that you can afford the loan and that you’re not taking on too much financial commitment. The more accurate and complete your documents, the smoother your application will be.